Now the big question-How?

This is probably a multi-million-billion dollar question. There are so many dynamics at play here to keep in mind that it will require a very careful, deliberate, and intelligent approach to get this right. I will try to cover some of the dilemmas RBI will have and will also share some questions to which we don’t have the answers now. Would love to know your thoughts on this. I will try to make this a series of shorter, bite-sized nuggets.

Let’s get started with the first of few. I guess you are aware by now that RBI kicked off the first pilot of e₹ with 9 Commercial Banks on the 1st of Nov 2022 (more about it here: https://economictimes.indiatimes.com/wealth/save/rbi-cbdc-digital-rupee-pilot-to-start-from-november-1-sbi-hdfc-7-other-banks-to-participate/articleshow/95205659.cms).

We need answers to a lot of different questions before we can begin to visualize how the future looks to be. The larger questions are around the Distribution, Technology, Value proposition, Security, and Privacy of e₹.

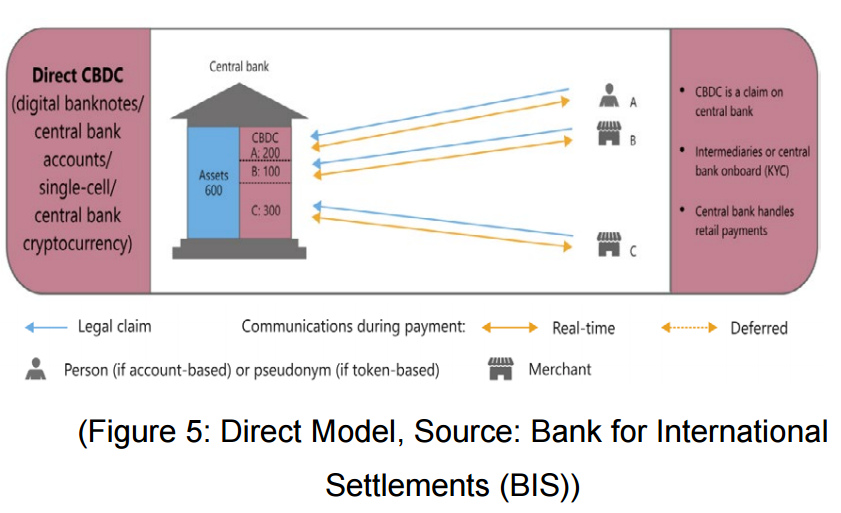

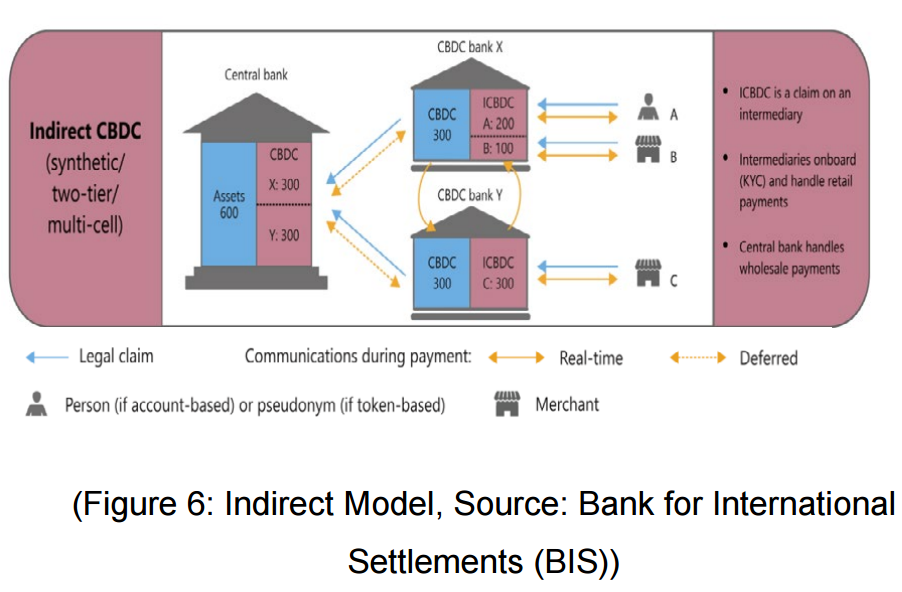

Let’s see what we know and what to expect on these fronts. In terms of the market for e₹, RBI will have 2 avatars of its CBDC- e₹-Retail (e₹-R) & e₹-Wholesale (e₹-W). The pilot is underway for the e₹-W. As mentioned in the last post, under how e₹ is different from the rupee balance you see in your savings bank account (or payment wallet)- it is issued by the RBI and is their liability. Let’s run with that idea for a minute, if RBI decides to allow me & you to have e₹ account, that account needs to be opened with RBI directly! Can you imagine the kind of infrastructure (digital & physical) such an undertaking would require? Also, it would be so redundant, given that for all these years the Govt & RBI have been trying to get Banks to expand their franchise and now by offering e₹ they will essentially be leaving out Banks from the transaction flow. So this is Dilemma No. 1- if to keep the distribution central or distributed

| Dilemma No 1 | RBI’s Answer | Rationale |

| Should Distribution be Direct or Indirect? | Both; Direct for Wholesale Segment and Indirect for Retail. | Wholesale will not require the kind of infra a Retail distribution will need, in terms of Account/Wallet creation, KYC, AML Checks, etc. |

Image Source: RBI’s Concept Note on CBDC

Leave a Reply