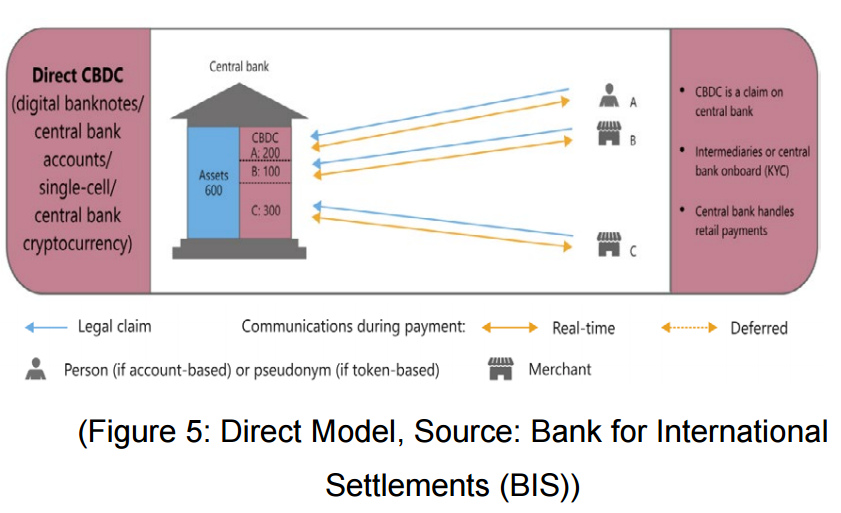

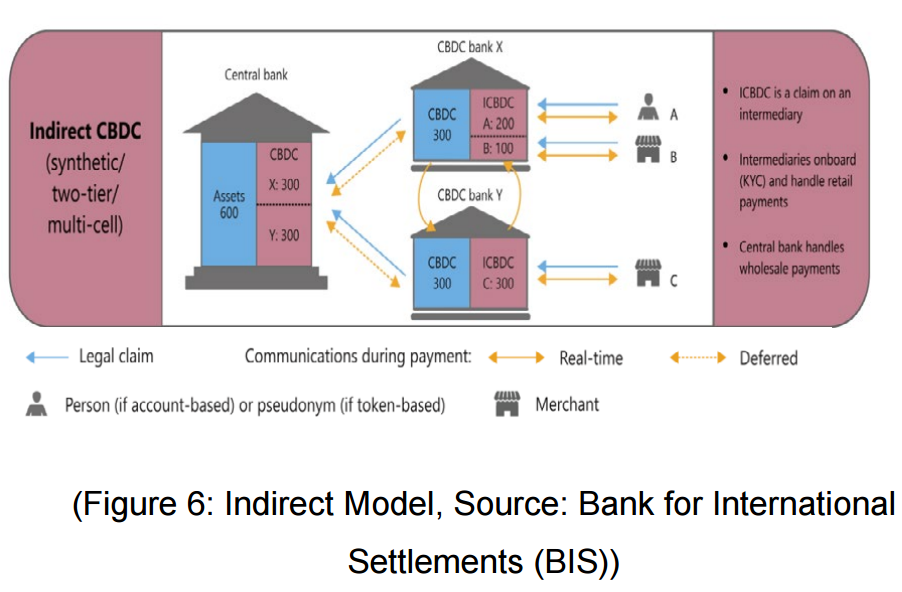

Picking up from where we left off in the last post. The indirect model

will pose certain challenges for the e₹-R such as the following:

- It will have almost no difference compared to the current rupee in

digital form (read your account balance in a savings account with any

commercial bank). - Your e₹ balances will not be updated with RBI in real-time thereby taking away one of the biggest USPs, i.e finality of settlement (the user will run the Settlement Risk in this model).

To overcome these challenges the model most likely to be implemented for the retail pilot is a Hybrid model. Before you ask what this hybrid model is, let’s see in some detail about all three models- direct, indirect & hybrid.

| Aspect | Direct | Indirect | Hybrid |

| Issuer | RBI | RBI issues to Intermediary for retail distribution | RBI issues to Intermediary for retail distribution |

| Liability | RBI | RBI | RBI |

| Operations | RBI | Intermediary Banks/Institutions | Intermediary Banks/Institutions |

| Who maintains the Ledger? | RBI | Intermediary Banks/Institutions | Intermediary Banks/Institutions & RBI |

| Settlement Finality | Yes | No | Yes |

The reason I think a Hybrid model suits better is that the indirect model does away with almost all the benefits that a Retail user might want from e₹. So what is

even the point? The Hybrid model, simply put is an indirect model with a messaging layer with it. Using this messaging layer, RBI will be able to keep a real-time ledger for each retail user. You can think of this as an e₹ account with a Commercial Bank along with a UPI-like layer to it which will update any transaction with RBI.

Now, dilemma no 2- this pertains to the token design. Should the e₹ have a token-based design like all major cryptocurrencies or should have an account-based design that enables book-keeping as well?

| Dilemma No 2 | RBI’s Answer | Rationale |

| Should the e₹ have a token-based design or an account-based design | Account-Based for the Wholesale segment for now and probably it will be Token-based for the Retail segment. | e₹ should offer the level of anonymity Cash offers. In the retail segment, RBI is trying to achieve lower Cash circulation by introducing e₹. To that end, a token-based e₹ will offer the holder, the right to spend without having to maintain a trail of the transactions. |

This is easier said than done! Such an approach (token-based) will also have lots of decisions to be made- such as whether should there be an amount ceiling for e₹-R, given the anonymity. More in the next post.