Sovereign Gold Bonds (SGBs) are financial instruments issued by RBI that allows investors to buy gold in a paperless form. They are denominated in grams of gold and are issued in multiples of one gram. The primary purpose of SGBs is to reduce the demand for physical gold and encourage people to invest in paper form instead.

One of the main advantages of SGBs is that they offer a safer and more convenient way to invest in gold. Unlike physical gold, SGBs are not subject to the risk of theft or loss. They are also easier to sell and can be traded on stock exchanges. In addition, SGBs offer a fixed rate of return, which is determined by the government at the time of issue. The current rate is 2.5% per annum, which is paid semi-annually.

Another benefit of SGBs is that they are exempt from capital gains tax on redemption. This means that investors do not have to pay any tax on their profit when selling their SGBs. This is a significant advantage, especially in a country like India where taxes on capital gains can be quite high.

SGBs are also attractive to investors because they offer a combination of both gold and debt. On one hand, they provide the security and stability of gold, which is considered a safe haven asset. On the other hand, they offer a fixed rate of return, similar to a debt instrument. This makes them an appealing option for investors looking to diversify their portfolios. It is important to note that SGBs are not the same as physical gold. They are simply a representation of gold and do not have any intrinsic value. This means that the price of SGBs is dependent on the market price of gold, which can fluctuate.

In conclusion, Sovereign Gold Bonds are a convenient and tax-efficient way for investors to buy gold. They offer a fixed rate of return, are easy to sell, and are exempt from capital gains tax. While they may not have the same intrinsic value as physical gold, they offer a combination of gold and debt, making them a good option for diversifying a portfolio.

What you read above is entirely written by #ChatGPT when asked- Write me a 300-word article on Sovereign Gold Bonds. There were 2 factual errors, which were edited out. Still, it makes a fantastic concise piece!

Later I asked #ChatGPT to compare Gold prices against Fixed Deposits over the last 20 years, which it couldn’t and so here comes the human part.

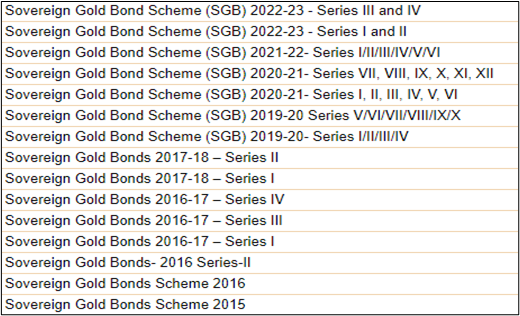

This product was launched by RBI in 2015 and since then has been offered multiple times over the years. Latest of which concluded on December

23, 2022.

The question is, does SGB make a good investment? I will answer this by

comparing it against Fixed Bank Deposits (FD). So in case you aren’t invested

in SGBs and hold FDs, do yourself a favor and read on.

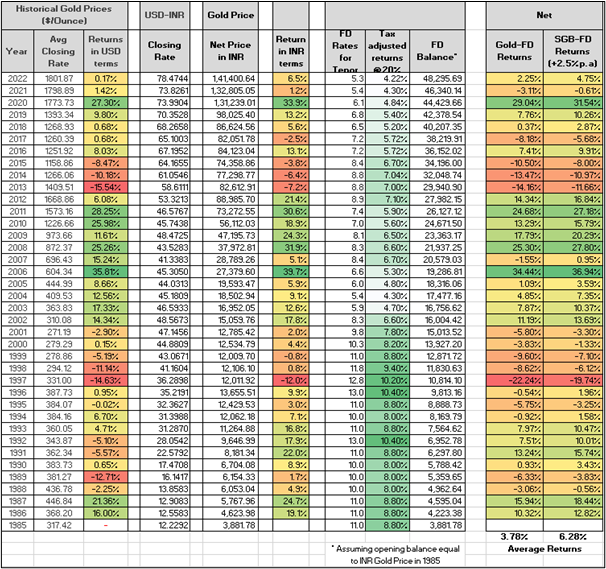

Since SGBs are intrinsically linked to Gold price, of course it is subject to market fluctuations and unlike FDs, might even deliver a negative return in certain years. FDs do deliver a guaranteed positive return but that statement is only valid if we are naïve to ignore inflation and only look at the nominal return instead of real return. If you subscribe to the macroeconomic idea that INR will keep depreciating against USD over longer periods, till there is an Inflation differential between the two economies. This return because of currency depreciation is in addition to any appreciation of Gold price (quoted in USD). To validate this, I looked at data for the period 1985-2022 and this is how it looks-

So Gold & SGBs in particular offer a better return over FDs. But is it enough of an incentive to subject yourself to the uncertainty vis-a-vis FDs? That’s a question one needs to evaluate based on investment goals and risk appetite.

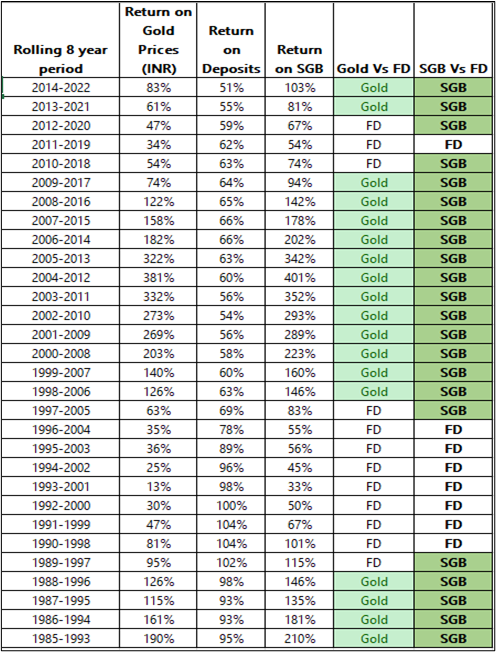

Now let’s do a comparison over a similar period. Since SGBs are an 8-year investment (there are options to exit before that but you lose on the tax benefit). Let’s look at the returns on both assets over rolling 8-year periods during 1985-2023.

You will see that out of 30 such periods, SGB emerges as the winner in 22 periods! That’s as good as an odd we can get. Also, SGBs on average return 75% higher over FDs over these 8-year periods. Now that’s a fantastic return and should be reason enough to persuade you to a reasonable allocation to SGBs over long-term FDs.

Now some nuances for the nerds:

- The FD rates taken for comparison are average FD rates for 5-year Deposits by leading 5 Banks in those years. Source: RBI website

- Tax payable on interest income is assumed to be 20%. Which depends on your tax bracket. A higher tax rate is an advantage to SGB.

- Interest rate on SGB is considered @2.5%, even though it was 2.75% for the first series.

- You may download the excel files here (Historical Data- SGB) and tweak the nos as you please.

- SGBs do not pose a reinvestment risk unlike FDs, depending upon the FD tenor you actually get from your bank.

- SGBs are an excellent tool if you want to take exposure to long-term currency depreciation (INR).

P.S.: I agree the title of this post was somewhat misleading (#ChatGPT) but at least it got you to read, what otherwise would have sounded drab to start reading. Who wanted another post on SGB after all!