Not being a wordsmith and these 2 are very different things! Short note on what’s what.

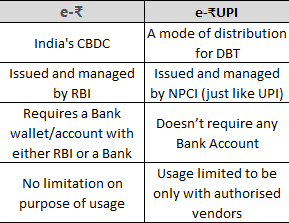

So, first e-Rupee or e-₹; this is what has been the talk of the town for over a month now. Simply put, it is India’s CBDC (Central Bank Digital Currency) launched by RBI, which is currently undergoing its pilot. {If you still wondering what is that, welcome to the blog and may I implore you to go through last few posts here. I beleive, that will be sufficient for you to gain a decent undertsanding of e₹. }. With e-₹ out of the way, what the hell is e-₹UPI!

Continuing with our long national tradition of creating clutter as much and wherever possible we have done it again! Jokes apart and to be fair, there wasn’t much room for having a better nomenclature for these 2. Anyways, this Seeta-Geeta business has got more than a handful mixing the two and serving it to people. The very reason I wanted to write on this, was because a few days back I came across this on youtube- https://youtu.be/My5pXiDCtU0 from Mr. Akshat Shrivastava. Great channel, superb content, and 1.35 mn Subs on Youtube alone! 10 days later this video has 304K views and 1500+ comments appreciating the content. The only hitch is that he has got it wrong, confusing e₹UPI as India’s CBDC.

Don’t get me wrong, I love his content and general take on life but this was a reason enough to make an effort to limit the misinformation. Enough digression, back to the subject.

e₹UPI was first announced by Prime Minister Narendra Modi on 2nd Aug 2021. Long before the e-Rupee (e₹) came into being.

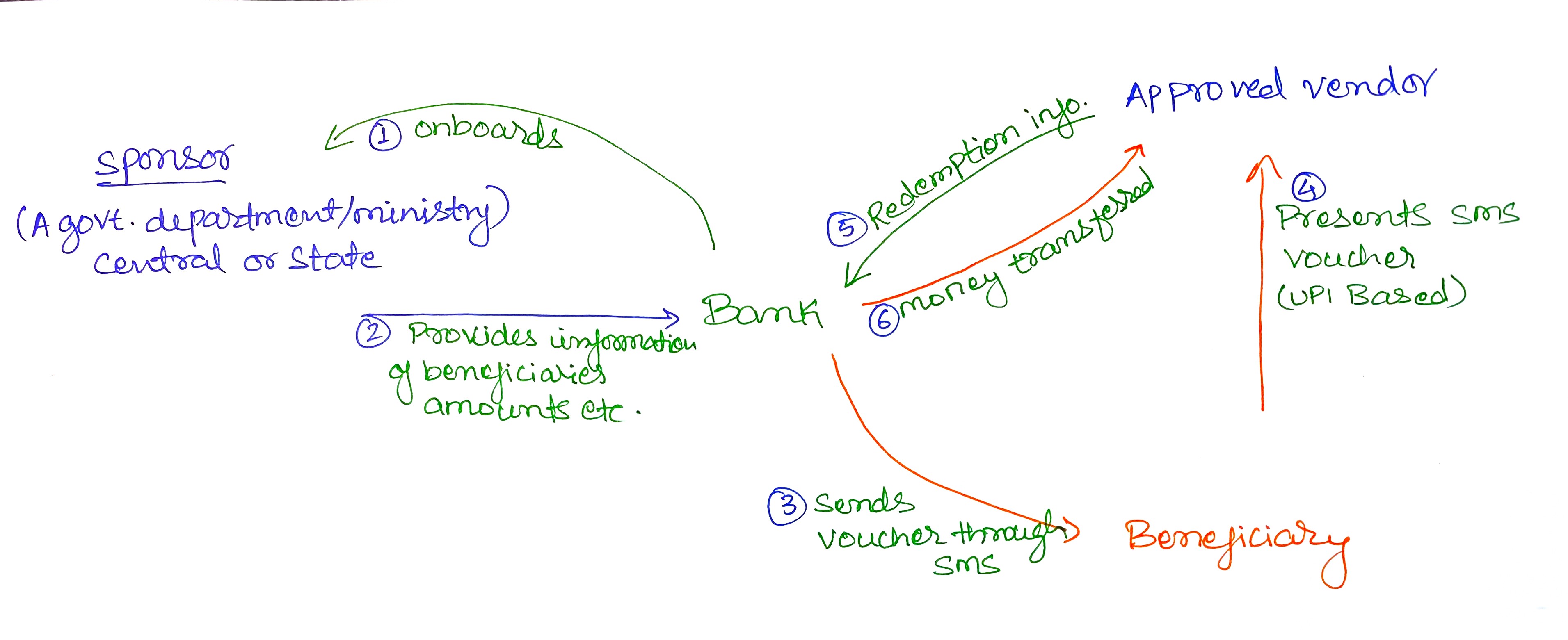

So what is e₹UPI? It is something which is intended to bring efficiency to Direct Balance Transfers (DBT) by the goverment. IT uses the UPI infra and hence the name e₹’UPI‘. Below is a simple 6 stage flowchart of how it will work.

(Ignore the colours, they don’t denote anything)

The process will start with a government, ministry, or department coming on board as a sponsor for a program. Let’s assume, the Dept of Basic Education for Uttar Pradesh decides to adopt e₹UPI for distributing the money they spend on each student to provide them with Books for each academic year. The department will provide the details of all such student beneficiaries, along with a mobile number, amount, validity, approved vendors etc to the Bank. The Bank’s portal integrated with NPCI, will issue SMS based, UPI-prepaid voucher to each beneficiary. Upon receipt of the voucher, the student can only redeem it at a pre-approved book-seller in the area.

This is how it is working in the current phase. However, it is expected that in the next phase it will allow for easier vendor selection/appointment and might open up a wider set of institutions to come on board as Sponsors. Imagine a private sector employer wants to reimburse its employees for certain healthcare expenses (eg: COVID vaccination). While the employer doesn’t want to go through the hassle of processing reimbursement but at the same time has to reasonably ensure the money is not spent for other purposes. Such an employer can come on-board e₹UPI and issue vouchers to its employees, who can only redeem their vouchers with Hospitals in their city. It has certain limitations in its current form but I think its benefits far outweigh any limitations. More on this in the next post.